-

Bank Accounts

Research By Category

Popular Accounts

Get a Recommendation

Managing Your Account

Bank Accounts For...

Account Selector

Account SelectorFind an account that's right for you:

-

Credit Cards

Research By Category

Popular Cards

Get a Recommendation

Managing Your Card

Credit Cards For...

-

Mortgages & Home Equity

Mortgage Solutions For...

Mortgage Rates

Mortgage Types

Managing Your Mortgage

Tools & Calculators

-

Personal Loans

-

Investments

+ Products and services may be offered by Royal Bank of Canada or by a separate corporate entity affiliated with Royal Bank of Canada, including but not limited to Royal Mutual Funds Inc., RBC Direct Investing Inc. (Member–Canadian Investor Protection Fund), RBC Global Asset Management Inc., Royal Trust Company or The Royal Trust Corporation of CanadaAdvice for Investors...

- Getting Started

- Building Your Wealth

- Getting Ready to Retire

- Living in Retirement

- Regaining Confidence

Investing & Wealth Planning

Types of Accounts

- Tax Free Savings - TFSA

- Retirement Savings - RRSP

- Retirement Income - RRIF

- Education Savings - RESP

- Disability Savings - RDSP

Online Investing

Investment Products+

- Guaranteed Investments - GICs

- Mutual Funds & Portfolio Solutions

- Savings Deposit

- Stocks and Bonds

- Exchange Traded Funds - ETFs

Tools & Calculators

Apply Now or Call 1-800-769-2511

Apply Now or Call 1-800-769-2511

[an error occurred while processing this directive]

Return Replacement Documents (RRDs) coming soon – Amendments to CPA Rule A10

The Canadian Payments Association Board of Directors recently approved amendments to CPA Rule A10 to permit financial institutions to create and use Return Replacement Documents (RRDs). These amendments allow financial institutions to make use of image technology and enhance efficiencies in the clearing system for payments items. These amendments come into effect in June 2011.

Financial institutions now have the option of creating and using RRDs for the purpose of returning refused cheques (for reasons such as NSF, post-dated etc). This is in addition to the two other optional return methods:

- Returning the original cheque.

- Using an Image Printout (for some extended time frame returns.).

RRDs are image-based, fully MICR-encoded documents, that allow financial institutions to return some dishonoured items more quickly. In some cases, this may allow a Negotiating Institution to charge a dishonoured item back to the depositor’s account earlier, and where appropriate, give the depositor the opportunity to escalate the issue to the Payor earlier.

To help reduce the potential of duplicate items in the clearing system, once the amendments to Rule A10 come into effect, items returned by any of the three optional return methods for any reason (other than those reasons used to adjust processing errors) will not be eligible for certification for the purpose of re-clearing. Payees will have the option of requesting a new cheque or another form of payment from the Payor, or sending the item on collection.

FAQs for Clients of Financial Institutions

- Is an RRD an official image?

- I have a payment item that is stamped with “Item Dishonoured”. What does this mean?

- Instead of the returned original payment item, I’ve received an image of the item, with return information printed on it. What is this, and why didn’t I get the original item back?

- Why are banks using RRDs? What’s the benefit?

- Will I always receive RRDs now, instead of original items?

- Will the bank certify an RRD so that I can re-deposit it?

- Without certification for re-clearing, how can I obtain payment?

- Can I still get a cheque certified?

- If I have received an RRD, can I get the original item back?

- What is the difference between an Image Printout and an RRD?

- What information does an RRD include?

1. Is an RRD an official image?

An RRD, if created in accordance with CPA Rules and Standards, is an official image. Pursuant to section 163.4(2) of the Bills of Exchange Act (BEA), an official image may be admitted as evidence in court for all purposes for which the original paper Cheque would be admitted as evidence.

2. I have a payment item that is stamped with “Item Dishonoured”. What does this mean?

This means that the item has been charged back to your account. The “Item Dishonoured” stamp indicates that payment for the item has been refused (for reasons such as NSF, post-dated, etc.) or cannot be obtained by the Payor’s financial institution.

The use of other stamps to identify returned items in the past, such as “Pursuant To” and “Payment Stopped” will be eliminated effective June 1, 2011, and the Payor’s financial institution will apply the “Item Dishonoured” Stamp when returning original payment items and Image Printouts.

3. Instead of the returned original payment item, I’ve received an image of the item, with return information printed on it. What is this, and why didn’t I get the original item back?

You have received a Return Replacement Document, also referred to as an RRD. An RRD is a MICR-encoded document that leverages image technology and enhance efficiencies in the return process. As of June 1, 2011, financial institutions may use RRDs for the purpose of return, in addition to the two other optional return methods: returning the original item or using an Image Printout (for extended timeframe returns).

4. Why are banks using RRDs? What’s the benefit?

RRDs, as image-based, fully MICR-encoded documents, offer financial institutions the ability to return some dishonoured items more quickly. In some cases, this may allow the Payee’s financial institution to charge an item back to the depositor’s account earlier, and where appropriate, give the depositor the opportunity to escalate the issue to the Payor earlier.

5. Will I always receive RRDs now, instead of original items?

As of June 1, 2011, depending on the reason for return, and the policies of the Payor’s financial institution, you may receive returns in one of three formats: original item, Image Printout, or RRD.

6. Will the bank certify an RRD so that I can re-deposit it?

As of June 1, 2011 items returned by any of the three optional return methods (original item, Image Printout or RRD), will not be eligible for certification for the purpose of re-clearing.

7. Without certification for re-clearing, how can I obtain payment?

Payees have the option of requesting a new cheque or alternate form of payment from the Payor, or, if offered by the Payee’s financial institution, presenting the item to be sent on collection.

8. Can I still get a cheque certified?

After June 1, 2011, financial institutions will no longer certify returned items (cheques) for the purpose of re-clearing. However, customers may still request certified items from their own financial institutions for the purpose of making a payment. In this case, the financial institution may either provide a certified cheque or offer a bank draft.

9. If I have received an RRD, can I get the original item back?

The availability of the original item will be dependent upon the internal policies of the Payor’s financial institution. The RRD, if created in accordance with CPA Rules and Standards, is an official image and may be admitted as evidence in court for all purposes for which the original paper Cheque would be admitted as evidence.

10. What is the difference between an Image Printout and an RRD?

An “Image Printout” is any paper output of a digital representation of the front and back of a payment item, produced by a CPA Member financial institution. An RRD is a form of Image Printout which meets the specifications in CPA Standard 013 - Return Replacement Document Design Standard, and which may be used for the purpose of return in accordance with CPA Rule A10.

11. What information does an RRD include?

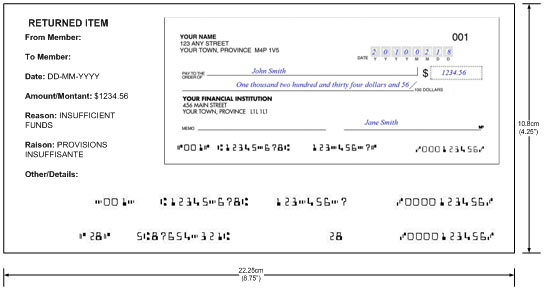

All RRDs must contain specific information on the front and back of the printed document, as per CPA Standard 013 – Return Replacement Document Design Standard. The minimum mandatory information elements are:

Front Layout:

- A scaled image of the front of the returned item. The image must maintain the aspect ratio of the original item.

- A primary MICR line at the bottom of the RRD which will include an RRD identifier code of “5” (for Canadian items only).

- A second MICR line printed above the primary MICR line used for clearing purposes. The second MICR line will be a reasonable representation of the MICR information encoded on the original item.

- The returning FI name and transit number.

- The negotiating FI name and transit number.

- The date the RRD is created.

- The reason for return, in English and French.

- The amount of the returned item.

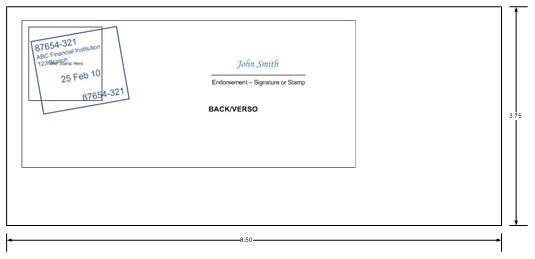

Back Layout:

- A scaled image of the back of the returned item. The image must maintain the aspect ratio of the original item. The image must be placed in such a way that it will not interfere with any stamps that may be applied by capture equipment when the RRD is being processed.

- SAMPLE RRD (Front)

- SAMPLE RRD (Back)

Top 10 Questions:

![]()

Royal Bank of Canada Website, © 1995-2026

To Top ![]() Text size:

Text size: