Tips for Making the Most of Your Retirement Savings

Check out our top tips to grow and maximize your retirement savings.

I’m Currently:

Have a plan.

If you’re new to saving and investing, creating a plan for retirement can feel overwhelming.. An advisor can take the guesswork out of choosing investments and help you create a realistic savings plan, so you know where you stand and how much you need to save.

Did you know? You can meet with an RBC advisor through video chat, by phone or in person to make a plan, talk strategy or to simply ask a question.

Be tax-savvy.

When it comes to saving for retirement, a Registered Retirement Savings Plan (RRSP) is a top choice for most Canadians. Here’s why:

- Your contributions can be deducted from your total income in the year you make the contribution, reducing the amount of income tax you pay (tax is deferred until you withdraw the funds from your RRSP).

- Deferring tax on your income allows you to contribute more into your RRSP, which allows it to grow faster. By the time you retire and withdraw the funds, you will probably be in a lower tax bracket than you are now while you are working and earning an income.

One thing to keep in mind—you can’t withdraw from an RRSP early without paying hefty penalty taxes (unless it’s for your first home1 or post-secondary education2). The good news is you can also open a Tax-Free Savings Account (TFSA), which lets you save for both retirement and other shorter-term goals. See how the RRSP and TFSA stack up.

Put your money to work.

Once you’ve opened an RRSP (and/or TFSA), make it work as hard as possible for you with regular, automatic contributions. By saving consistently (weekly, monthly, etc.) your money could grow faster over time.

- You decide how much to save and how often—weekly, bi-weekly, monthly—it’s up to you

- Contributions are automatically debited from your bank account (at RBC or another financial institution)

- You can change how much you want to save, how often you contribute, and stop or pause your contributions at any time

Tip: Set your automatic contributions to coincide with every paycheque.

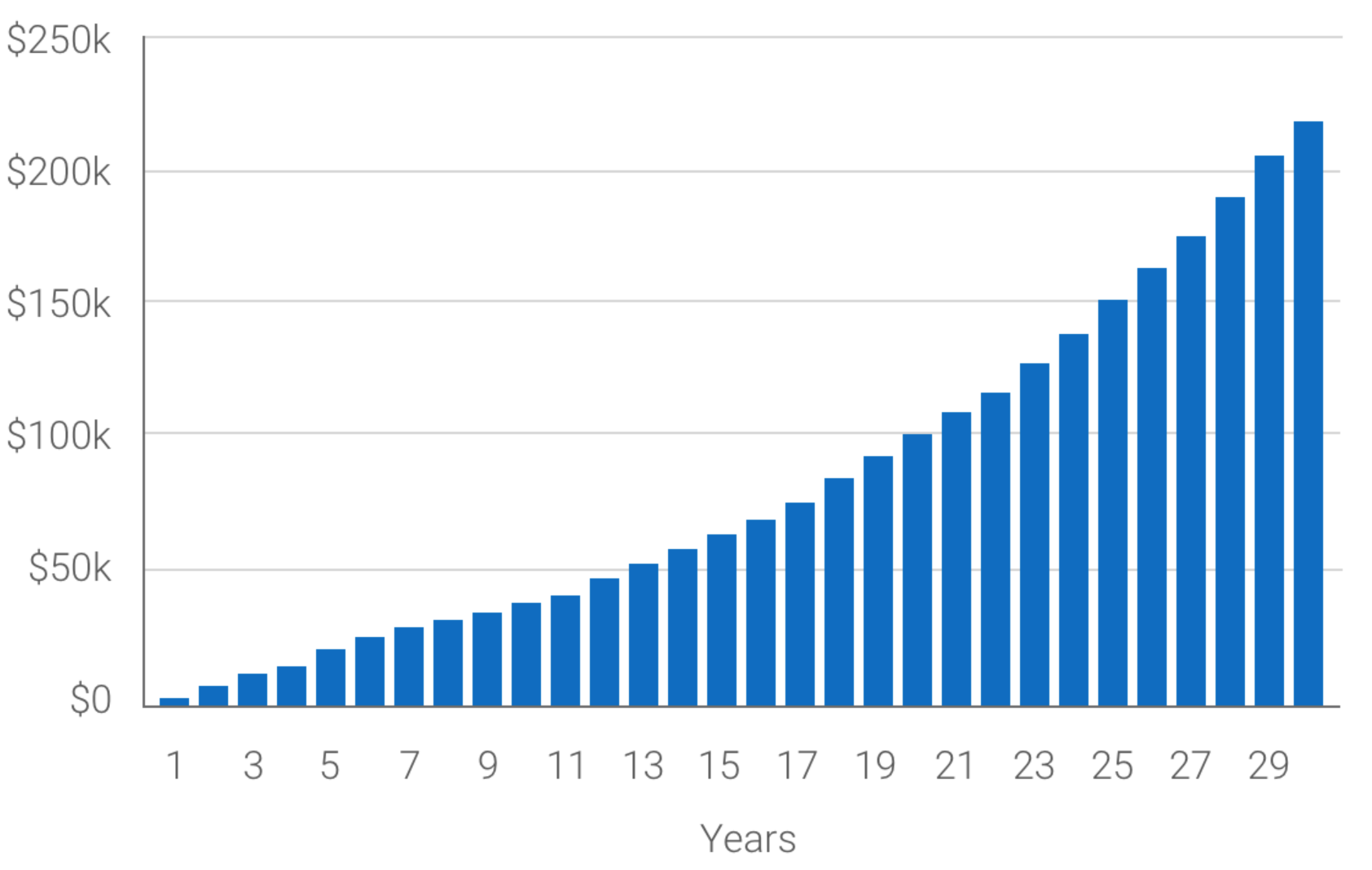

Putting just $50 per week in an RRSP adds up:

Try the RRSP Calculator now to see how quickly your money can grow.

The chart shows how $50 contributed weekly, earning a 6% rate of return, can grow to over $218,000 over 30 years. Calculations are for illustrative purposes only and are not intended to reflect future values or returns on investment from any mutual fund investment.

Start somewhere.

Feel like you can’t put much away right now? Start with what you have. Anytime you have extra cash (a tax refund, for example) you can always contribute more.

RBC client? Use NOMI Find & Save on the RBC Mobile app to help save money you didn’t know you had. It’s a free digital savings account that learns your transaction patterns, finds extra dollars in your cash flow and automatically moves them to savings. Once you have a little bit saved, you can contribute this amount to an RRSP!

Stay on track with MyAdvisor.

If you’re an RBC client, you’ve also got exclusive (and free) access to MyAdvisor, a digital service that can help you start saving for retirement and also help you stay on track.

MyAdvisor is a digital service that combines interactive planning tools and advice from a live advisor to help you be better prepared for retirement.

- See what you have with more certainty. MyAdvisor shows you how you’re doing with powerful visuals and forecasts of your goals, net worth and cash flow.

- Link outside accounts for a complete picture. Have savings and investments outside of RBC? MyAdvisor lets you quickly link them for an up-to-date look at your money.

- Receive personalized advice. Meet with a live advisor through video chat, by phone or in person to review your retirement plan, talk strategy or to simply ask a question.

- Make changes to your retirement savings plan at any time. Want to see a recommendation from your advisor or make a change to your plan? Simply log in to your MyAdvisor dashboard.

- Stay on track toward your goal with email alerts. Progress alerts let you know whether you need to adjust the amount you are saving in order to reach your retirement goal.

- Get started in a few simple, hassle-free steps. In minutes, you’ll have an idea of where you stand, see recommendations to help you grow your savings, and be able to book a one-on-one with an advisor.

Sign in to RBC Online Banking and try MyAdvisor today.

Tools and Resources

FAQs on Retirement Planning

The answer to this question will be different for everyone. For example:

- How much savings (and debt) do you have now? How are your investments performing?

- What kind of lifestyle do you want in retirement? Do you want to travel the world—or start a new part-time career?

- Will your mortgage and other debt be paid off?

- When do you want to retire—and how much time do you have left to save?

Working with an advisor or financial planner is the best way to understand how much you’ll need to reach your unique goals.

When it comes to saving for retirement, a Registered Retirement Savings Plan (RRSP) is a popular choice for most Canadians. A Tax-Free Savings Account (TFSA) can also be used to save for retirement, but it gives you the flexibility to save for shorter-term goals, too.

Here are a few ways the RRSP and TFSA stack up:

- Your savings in an RRSP grow tax-deferred while your savings in a TFSA grow tax-free.

- RRSP contributions are tax-deductible, helping you to pay less tax in your earning years. TFSA contributions are not tax-deductible.

- Your RRSP contribution limit is based on your employment income. You can continue to contribute to your RRSP so long as you have contribution room available. With a TFSA, you can contribute even if you aren’t working and earning.

- You can’t keep saving in your RRSP after age 71—a TFSA lets you make contributions for life.

- Withdrawals from a TFSA are never taxed. Withdrawals from an RRSP are taxed the year you withdraw the money.

To compare more features and benefits, see TFSA vs RRSP vs eSavings.

Most people think of 65 as the standard retirement age since Canadians can start collecting Old Age Security (OAS) and Canada Pension Plan (CPP)/Quebec Pension Plan (QPP) benefits at that time. (You can also start taking CPP/QPP sooner, but your payments will be reduced.)

In reality, 64.3 was the average retirement age for all Canadian retirees in 2019. Self-employed Canadians retired the latest, at age 67.1, and those who worked in the public sector (a government agency, for example) retired the earliest at age 62.6.3

Individuals who work with an advisor have been shown to have almost four times the assets of those who don’t work with an advisor!4 An RBC advisor can help you:

- Determine whether you are saving enough to enjoy the type of lifestyle you want in retirement

- Make sure your money is working as hard as possible for you

- Adjust your investments as needed to keep your retirement plan on track

You can meet with an RBC advisor through video chat, by phone or in person to make a plan, talk strategy or to simply ask a question.

Want Help Deciding How to Invest? Let’s Connect.

Talk to an advisor for one-on-one investment advice, help making a plan and more.

Things our lawyers want you to knowThings our lawyers want you to know