An RRSP is a registered investment account that lets you save for your retirement by deferring

taxes on your investment earnings. This means more of your money can stay invested and grow

faster.

An RRSP also helps you lower your tax bill today, by allowing you to deduct RRSP

contributions from your taxable income. By the time you retire you will likely be in a lower

tax bracket, so withdrawals are taxed at a lower rate than today.

Registered Investment Accounts

Registered investment accounts offer unique tax advantages to help you save for the

future. For example, the Registered Retirement Savings Plan (RRSP) lets you deduct your

contributions from your taxable income now and defer the taxes until you withdraw that

money in retirement, while investment income you earn in a Tax-Free Savings Account

(TFSA) is never taxed. The features, benefits and rules for registered accounts are

determined by the Government of Canada.

Here’s why nearly half of Canadians polled invest in an RRSP1:

Use an RRSP to save for retirement while also saving for anything in a TFSA

Contributions reduce your annual income, lowering your tax bill

Taxes on your investment income are only paid when withdrawn

You can borrow money from your RRSP to go to school2 or

buy your first home3 without penalty, provided

it is repaid within the required time

You can make up for missed contribution room from previous years

Exclusive Benefits When You Invest With RBC

Free Digital Tools to Help You Plan & Save

See all your money in one place, get tips and save automatically with smart tools

such as MyAdvisor and NOMI Find & Save.

Advice When You Need It

Speak with an advisor in-person, by phone or over video - whether you're investing

$50 or $5,000.

How an RRSP Works

Here's how an RRSP can help you save for a comfortable retirement:

An RRSP is a type of registered investment account, which means you can

hold income-generating investments in it versus just cash (like a

savings account).

The types of investments you can buy in your RRSP depend on where you

open an account. You also want to consider your appetite for risk when

choosing investments.

RBC Royal Bank: Ideal if you want investment advice and access to

an advisor – in-person, by

phone or over video.

Tip: At RBC, you can open an RRSP

with any amount you are comfortable with. Just keep your contribution

(deduction) limits in mind.

Since the investment income you earn in an RRSP (interest,

dividends or capital gains) is not taxed until it’s

withdrawn, it has the opportunity to grow faster than it would in a

non-registered account.

Another way to save faster is by setting up regular (weekly, monthly,

etc.) automatic

contributions into your RRSP.

Dividend:

Distribution of a portion of a company's earnings, decided by the

board of directors, to a class of its shareholders. Dividends

are often quoted in terms of the dollar amount each share

receives (dividends per share or DPS).

Capital Gains or Capital Loss:

Profit or loss from the sale of real estate, stocks, mutual

funds, and other holdings classified as capital assets under the

federal income tax legislation. The tax treatment of capital

gains is different from other types of investment income such as

dividends and interest income.

You decide how much to save and how often—weekly, bi-weekly,

monthly—it’s up to you.

Tip: Keep your available RRSP contribution (deduction) room

in mind when setting up automatic contributions.

Contributions are automatically debited from your bank

account (at RBC or another financial institution).

You can change how much you want to save, how often you

contribute, and stop or pause your contributions at any

time.

By December 31 of the year you turn 71, you must stop contributing to

your RRSP and convert it to an income option such as a Registered

Retirement Income Fund (RRIF) or annuity.

A RRIF is like an extension of your RRSP, but instead of putting money

in, you withdraw money to use throughout retirement.

You may be able to borrow from your RRSP for other purposes, as well.

Here are a few things to know:

Withdrawals from your RRSP or RRIF are considered part of your

taxable income.

Withdrawals can affect your eligibility for government benefits,

such as Old Age Security (OAS).

Early withdrawals from your RRSP will raise your tax bill and have a

withholding tax deducted upfront.

The Home

Buyers’ Plan may let you borrow up to $60,000 from your RRSP

to buy your first home.3

The Lifelong Learning

Plan may let you borrow up to $10,000 in a calendar year (to

a maximum of $20,000) from your RRSP to cover training or education

for yourself or your spouse.2

Numbers to Know

$33,810

2026 RRSP deduction limit—or 18% of your earned income the previous year—whichever is lower

$60,000

Maximum amount you may be able to borrow from your RRSP to buy your first home3

71

The age at which contributions stop and you need to convert your RRSP to an income

option (like a RRIF)

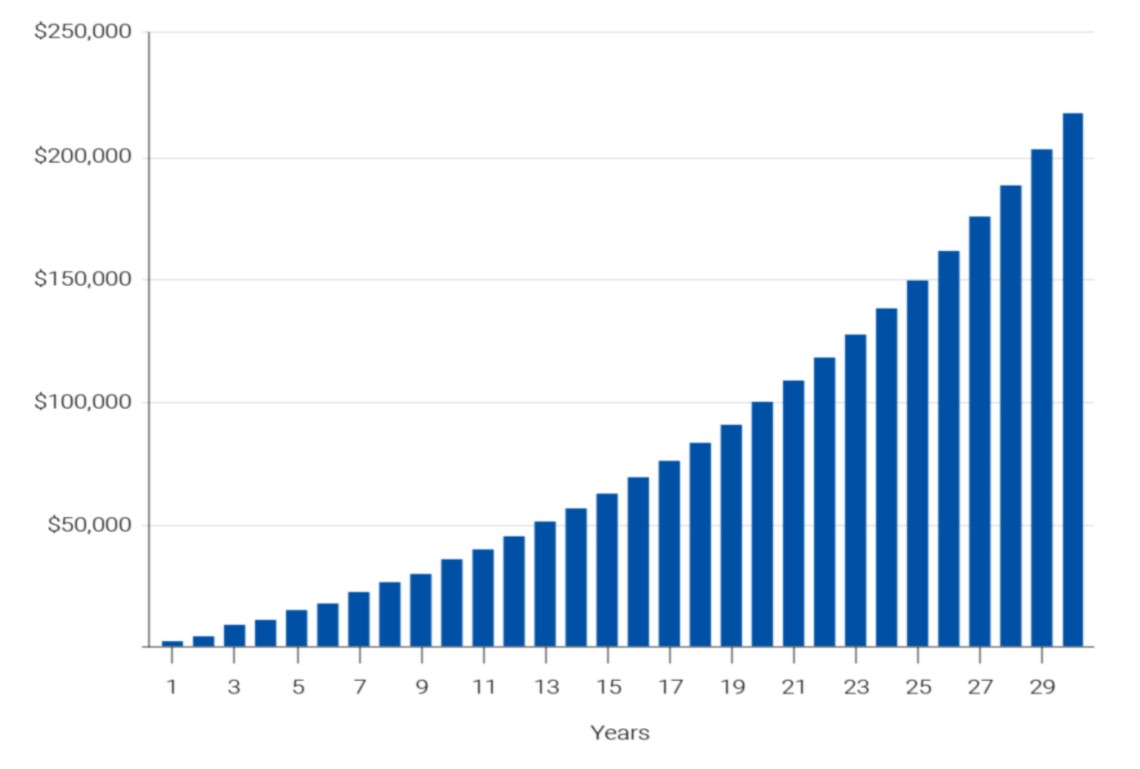

See How Saving Regularly Could Help Your RRSP Grow

The following chart shows how $50 contributed weekly, earning 6% interest, can grow to over $218,000 over 30 years.

The following chart shows how $50 contributed weekly, earning 6% interest, can grow to over $218,000 over 30 years.

RRSP Calculator

See how convenient it is to save with regular, automatic contributions to your RRSP*.

Years

Enter a number from 1 to 50

$Dollars

Enter a number between 25 to .Enter a number between 25 to

Although you can take money from your RRSP before you retire, it's not

recommended because of the negative impact on your retirement plan—

taxes on withdrawals are usually higher during your working years, plus

you lose the contribution room used to make the original contribution.

Withdrawals must be declared as income on your tax return at the end of

the year and withholding tax will also be deducted from the amount you

withdraw.

If you decide you would like to withdraw from your RRSP, you can do so in

several ways:

There is a service fee of $150.00 for the transfer of property from an

RRSP to a company that

is not a subsidiary of Royal Bank of Canada. This fee is subject to

change. In the event

this fee changes or new fees are introduced, RBC will notify clients by

mail or

electronically at least 30 days before the effective date of the change.

Individual RRSP: The most common type of RRSP is a plan registered

in your name. The investments held in the plan and all the tax

benefits belong to you.

Spousal RRSP: When you contribute to a spousal RRSP, you still get

the tax deduction but the plan is registered in your spouse's name.

(Your spouse's contribution limit to his or her own plan is not

affected.) It’s a great income-splitting option if one of you earns

more than the other.

Locked-in RRSP: If you leave your employer before you retire, you

may be offered the option to manage your vested pension funds. A

Locked-in RRSP—Locked-in Retirement Account (LIRA) in some

provinces—enables you do this.

Group RRSP: Some employers offer a Group RRSP, a collection of

individual RRSPs for the company’s employees. As an employee, your

RRSP contributions are taken from your pre-tax pay through payroll

deductions, reducing your tax burden immediately.

At RBC, you can open an RRSP at:

RBC Royal Bank: Ideal if you want investment advice

and access to an advisor—in-person, by phone or over video. Choose

from mutual

funds, GICs

and savings

deposits to hold in your RRSP.

RBC

Direct Investing : Ideal if you want to trade

and invest yourself using powerful online tools and resources.

Choose from stocks, options, Exchange-Traded Funds (ETFs), mutual

funds, bonds and GICs to hold in your RRSP.

RBC

InvestEase : Ideal if you want to invest

without having to research a single investment. Answer a few

questions and RBC InvestEase will match you to a

professionally-built ETF portfolio.

The types of investments you can buy in your RRSP depend on where you

open an account. You also want to consider your appetite for risk when

choosing investments.

RBC Royal Bank: Offers mutual funds,

GICs and savings

deposits. Ideal if you want investment advice and access to

an advisor—in-person, by phone or over video.

RBC

Direct Investing : Offers stocks, options,

Exchange-Traded Funds (ETFs), mutual funds, bonds and GICs. Ideal if

you want to trade and invest yourself using powerful online tools

and resources.

RBC

InvestEase : Offers ETF portfolios designed for

different investors (each portfolio holds a diverse mix of ETFs).

Ideal if you want to invest without having to research a single

investment.

Although you can take money from your RRSP before you retire, it's not

recommended because of

the negative impact on your retirement plan due to taxes on withdrawals.

Withdrawals must be

declared as income on your tax return at the end of the year and

withholding tax will also

be deducted from the amount you withdraw.

If you decide you would like to withdraw from your RRSP, we encourage you

to first use our online booking tool to schedule a time to speak

with an advisor by

phone.

Yes, you can use your RRSP funds to cover an emergency situation.

However, there is a tax

consequence to doing so and an impact on your retirement plan. Any

withdrawal is considered

taxable income for the year and a withholding tax will be deducted

upfront when you withdraw

the funds.

Yes, you can set up automatic contributions to your RRSP using funds

from your chequing or savings account at RBC or another financial

institution.

Try the RRSP

calculator to see the benefits of regular, ongoing

contributions.

This amount varies per person.

To find out the exact amount you can contribute for the current year,

check your most recent Notice of Assessment from the CRA, which you can

access through the “My Account” function on the CRA website.

As a guideline, your allowable RRSP contribution for the current year is

the lower of:

18% of your earned income from the previous year

The maximum annual contribution limit for the tax year

The remaining limit after any company-sponsored pension plan

contributions

Below are the maximum annual RRSP contribution limits from 2013-2021

Royal Bank of Canada and Royal Mutual Funds Inc. (RMFI) make no warranties,

express or implied, as to the accuracy or completeness of the information

contained herein.

Royal Bank of Canada and RMFI shall not be liable for any losses or damages

arising from any errors or omissions in information contained in this

calculator.

Financial planning and investment advice are provided by RMFI. RMFI, RBC Global

Asset Management Inc., Royal Bank of Canada, Royal Trust Corporation of Canada

and The Royal Trust Company are separate corporate entities which are

affiliated. RMFI is licensed as a financial services firm in the province of

Quebec.

Information about the Registered Retirement Savings Plan is based on what is

currently available from the Canadian government and can be subject to change.

With the “GoSmart $50” offer (the ‘Offer’), you could receive a cash reward of C$50 when you open your first GoSmart Account(s) with RBC Direct Investing.

To qualify, you must -

Open your first GoSmart account(s) with RBC Direct Investing between January 20, 2026, and July 31, 2026, (inclusive) by scanning the QR code for the Offer or following a promotional link for the Offer.

Contribute a minimum of C$500 (Five Hundred Canadian Dollars) to your new GoSmart account(s) before April 2, 2027.

Be a Canadian resident and at least the age of majority in your province/territory at the time of opening your first GoSmart account.

You will receive the C$50 cash reward in your first GoSmart account within 7 (Seven) days of meeting the above qualification criteria. This Offer is exclusively for GoSmart accounts, but may be combined with other RBC Direct Investing promotions. Additional terms and conditions may apply to opening an account with RBC Direct Investing (including a GoSmart Account) which include, without limitation, the requirements set forth in RBC Direct Investing’s Operation of Account Agreement. This Offer may be modified, restricted, withdrawn or extended at any time without notice at the sole discretion of RBC Direct Investing and is subject to the full terms and conditions of the Offer.

1)

RBC

2020 Financial Independence in Retirement Poll. Findings from the 30th

annual RBC RRSP Poll, conducted by Ipsos from December 10 to 17, 2019 on behalf

of RBC Financial Planning, through a national survey of 2,000 Canadians aged 18+

who completed their surveys online. Quota sampling and weighting are employed to

balance demographics to ensure that the sample's composition reflects that of

the adult population according to Census data and to provide results intended to

approximate the sample universe. The precision of Ipsos online polls is measured

using a credibility interval. In this case, the poll is accurate to within

±2.2 percentage points had all Canadian adults been polled. All sample

surveys and polls may be subject to other sources of error, including, but not

limited to coverage error, and measurement error.

2)

Under the Lifelong Learning Plan, you can withdraw up to $10,000 per calendar

year for your own or your spouse's full–time training or post–secondary

education.

The total amount that can be withdrawn is $20,000 each with withdrawals over a

maximum of four consecutive years.

At least 10% of the amount borrowed must be repaid each year, over a maximum

period of 10 years.

3)

You can withdraw up to $60,000 from your RRSP to buy your first home under the Home Buyer’ Plan. To be eligible, you must be a Canadian resident and considered a first-time homebuyer. The funds must have been on deposit at least 90 days before you withdrew them, and a signed written agreement to buy or build a qualifying home is required. Funds withdrawn under the HBP must be repaid to their RRSP over a 15-year period. At least 1/15 of your withdrawal must be repaid to the RRSP each year. The repayment period begins as of the second year after the first withdrawal was made under the Home Buyers Plan (HBP).

For withdrawals between January 1, 2022 and December 31, 2025, the repayment period begins as of the fifth year after the withdrawal was made. For details see Canada Revenue Agency Home Buyers’ Plan

4)

RBC Direct Investing Inc. and Royal Bank of Canada are separate corporate

entities which are affiliated. RBC Direct Investing Inc. is a wholly owned

subsidiary of Royal Bank of Canada and is a Member of the Canadian Investment Regulatory Organization and the Canadian Investor Protection Fund.

Royal Bank of Canada and certain of its issuers are related to RBC Direct

Investing Inc. RBC Direct Investing Inc. does not provide investment advice or

recommendations regarding the purchase or sale of any securities. Investors are

responsible for their own investment decisions. RBC Direct Investing is a

business name used by RBC Direct Investing Inc.

5)

RBC InvestEase is a restricted portfolio manager providing access to model

portfolios consisting of RBC iShares ETFs with each model portfolio holding up

to 100% of RBC iShares ETFs. RBC iShares ETFs are comprised of RBC ETFs managed

by RBC Global Asset Management Inc. (RBC GAM) and iShares ETFs managed by

BlackRock Canada Limited (BlackRock Canada). RBC GAM and BlackRock Canada have

entered into a strategic alliance to bring together their respective ETF

products under the RBC iShares brand, and to offer a unified distribution

support and service model for RBC iShares ETFs.

Other products and services may be offered by one or more separate corporate

entities that are affiliated to RBC InvestEase Inc., including without

limitation: Royal Bank of Canada, RBC Direct Investing Inc., RBC Dominion

Securities Inc., RBC Global Asset Management Inc., Royal Trust Corporation of

Canada and The Royal Trust Company. RBC InvestEase Inc. is a wholly-owned

subsidiary of Royal Bank of Canada and uses the business name RBC InvestEase.

The services provided by RBC InvestEase are only available in Canada.

6)

Assets in an RRSP must be Qualified Investments under the Income Tax Act. If the

TFSA holds non-Qualified Investments, it could be subject to tax.

7)

Real-time streaming quotes are available on stocks and ETFs for all clients.

Real-time streaming quotes are also available on options and over-the-counter

(OTC) securities for Royal Circle and Active Trader clients, upon accepting the

terms and conditions of all exchange agreements on the RBC Direct Investing

online site.