TLDR

-

An emergency fund is a financial cushion that can help you get through tough times, such as losing your job.

-

Having an emergency fund can help you avoid debt, reduce stress and preserve your long-term savings.

-

Your emergency fund should contain enough money to cover three to nine months’ worth of living expenses, depending on your personal situation.

-

By organizing your budget and setting aside small amounts to contribute regularly, you can be on your way to building your own emergency fund.

You’ve got a budget, and you stick to it. But have you ever thought about how you’d cover expenses in a crisis, such as a job loss, illness or major home repair? That’s where an emergency fund comes in. It’s money you set aside to help you weather life’s storms.

What is an emergency fund?

An emergency fund is money you set aside to help with unexpected life events or large expenses, such as job loss, prolonged illness, major auto repairs or unplanned home renovations, like replacing a roof damaged by a storm. These savings are separate from planned spending and “fun” things like vacations or a new car. Those expenses should be covered by your regular budget.

An emergency fund is an important part of your financial plan because, in a crisis, it can help you:

-

Avoid debt: When you’re strapped for cash, it may feel easy to cover costs with a credit card. But if you can’t pay off the balance right away, the debt could continue to grow due to interest charges. Having an emergency fund ready may help you avoid the extra costs of carrying long-term debt.

-

Reduce stress: Research shows that about half of Canadians lose sleep over money. Having an emergency fund in place can offer peace of mind and help protect you from financial hardship.

-

Protect your savings: When faced with emergency expenses, some people dip into retirement savings or kids’ education funds. This can jeopardize future plans. An emergency fund can help preserve your savings, so you can continue working towards your life goals.

When to use your emergency fund

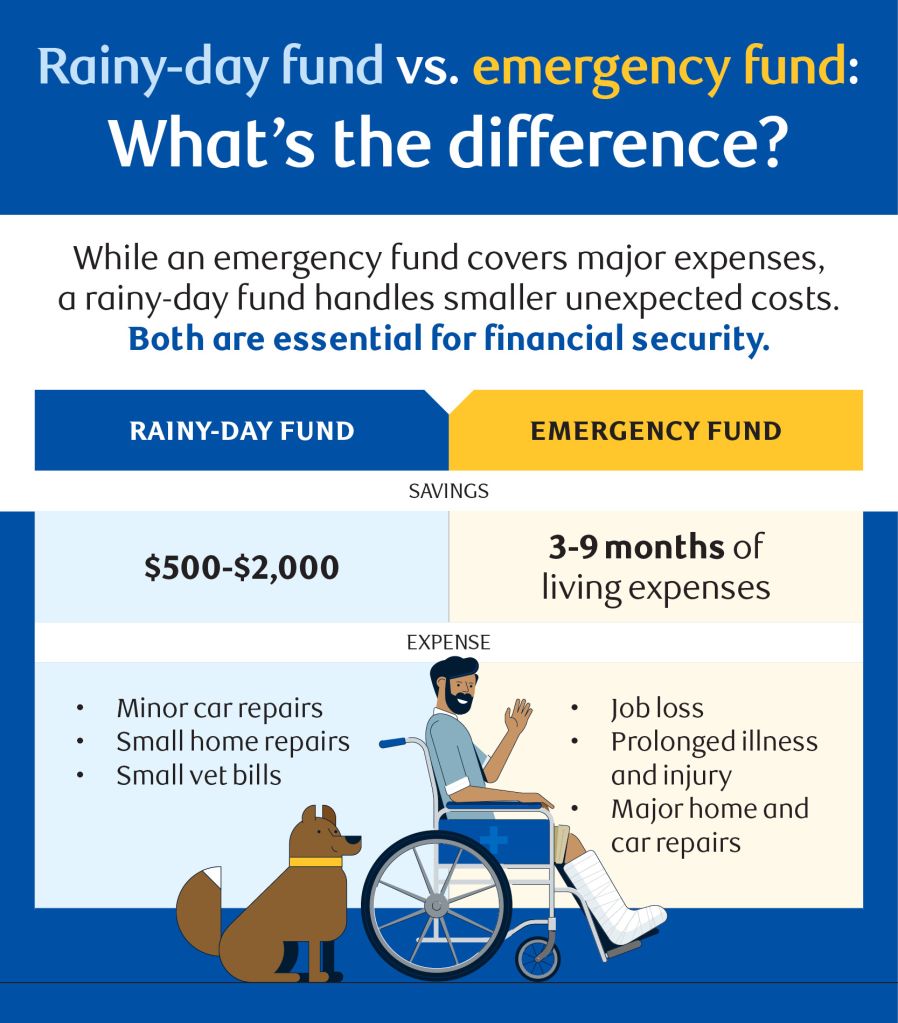

Losing your job and being unable to make rent is a worst-case scenario, but lesser unexpected costs might also pop up from time to time. These expenses fall under the umbrella of a rainy-day fund. Both are important for your financial strategy.

Here’s the difference between the two.

| Rainy-day fund | Emergency fund |

| Costs: $500-$2,000 Minor car repairs Small vet bills Small home repairs | Costs: 3-9 months of living expenses Job loss Prolonged illness and injury Major home and car repairs |

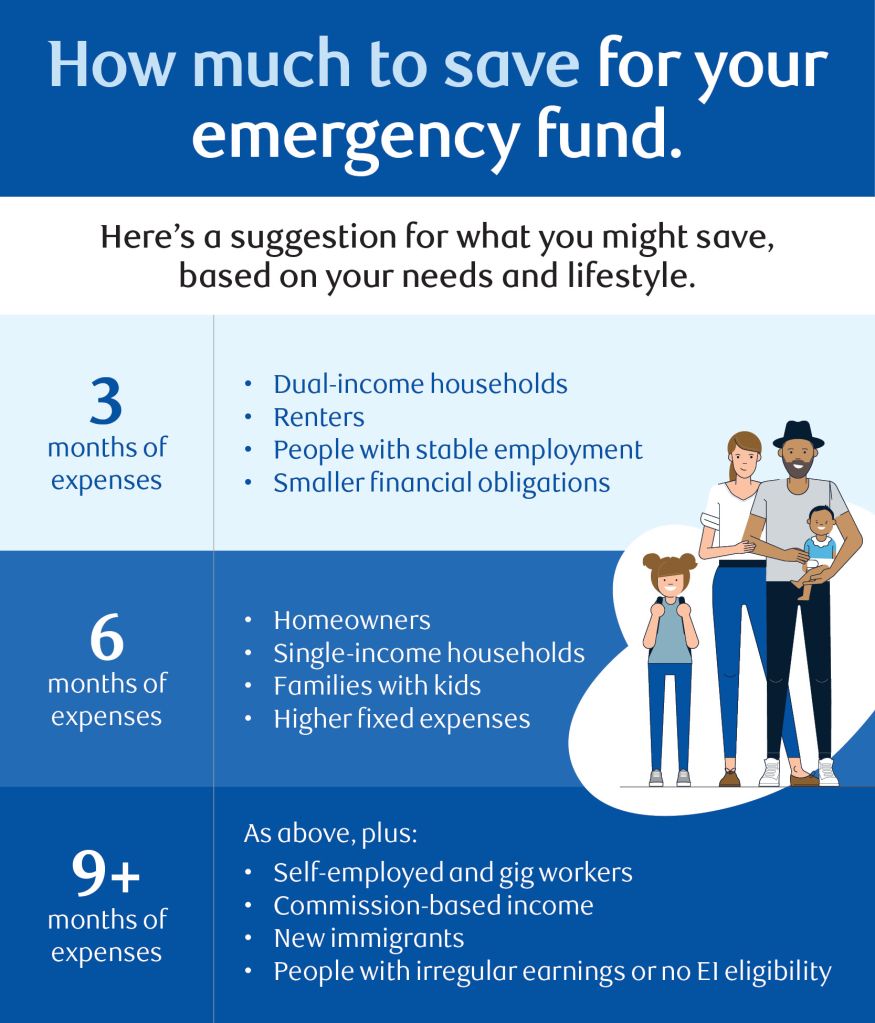

How much should you save? Use the 3-6-9 emergency fund rule

The exact amount you should save will depend on your personal situation. The general recommendation is that an emergency fund should cover three to nine months’ worth of expenses. Start by considering how long it might take you to earn income again after a job loss. Here’s a suggestion for what you might save, based on different needs and lifestyles.

| 3 months of expenses | Dual-income households Renters People with stable employment Smaller financial obligations |

| 6 months of expenses | Homeowners Single-income households Families with kids Higher fixed expenses |

| 9+ months of expenses | As above plus: Self-employed and gig workers Commission-based income New immigrants People with irregular earnings or no EI eligibility |

While building an emergency fund to cover more than three months of expenses may be challenging, don’t get discouraged. Even small amounts of savings can be beneficial. The key is to develop a consistent saving habit.

How to calculate your emergency fund amount

To figure out how much you should save, calculate the living costs you’d need to cover if something unexpected happened.

Start by tracking your regular monthly expenses, such as:

-

Housing: Rent or mortgage payment, property taxes and condo fees

-

Utilities: Electricity, water, natural gas/heating and trash collection

-

Communications: Mobile phone plan and home internet

-

Insurance: Health, auto, homeowners/renters and life insurance

-

Transportation: Car payments, public transit passes and gas

-

Childcare/Education: Daycare costs, school tuition, or student loan minimum payments

-

Groceries: Food and household supplies

-

Medical: Medications and healthcare not covered by provincial insurance

Next, factor in other costs that may not be included in an average month, ad hoc expenses such as kids’ summer camps, holiday expenses or bi-monthly tax bills.

Once you’ve calculated your average monthly expenses, multiply that by the number of months you need your emergency fund to cover. That’s your target savings amount.

Where to keep your emergency fund

It’s a good idea to keep your emergency fund in its own account, separate from the money you use to cover day-to-day expenses. That way, you won’t be tempted to dip into it.

You want the money to be liquid – in other words, easily accessible when you need it. Ideally, it should earn you more money as you save it. That’s why a chequing account, which usually pays little to no interest, may not be the best place to keep it.

A high-interest savings account (HISA) or cashable GIC may offer liquidity and higher interest rates to help you save more. You have the option to keep these inside a Tax-Free Savings Account (TFSA), which means you won’t have to pay income tax on the interest you earn. Make sure you don’t exceed your TFSA contribution maximum. Learn how to set up a HISA and compare savings accounts here.

Use the RBC Savings Calculator to help plan your contributions and see how your money may grow over time.

How to build your emergency fund step by step

Building an emergency fund takes time and dedication, but it’s easy to get started. Follow these steps to set yours up.

Step 1: Set a goal

-

Calculate how much you’ll need in your emergency fund.

-

Decide on a monthly or per-paycheque amount to put toward that goal.

Step 2: Create or update your budget

-

Organize your finances so you can make regular contributions to your emergency fund while still meeting other expenses.

-

Identify where you might cut back temporarily to reach your goal faster.

Step 3: Open a separate account

-

Consider opening a separate account (like a HISA or TFSA as mentioned above) to keep your savings separate while providing easy access to your funds. A savings account with higher interest may be a good choice.

Step 4: Automate your savings

-

Build your account by setting up regular, automatic contributions.

-

Time your transfers to your pay periods to make saving even easier.

-

Learn more about setting up an automated savings plan.

Tip: Contributing lump sums, such as work bonuses, cash gifts or tax refunds, is a good opportunity to get closer to your goal.

How to rebuild your emergency fund after you use it

Start saving again as soon as possible. Contributing even small amounts can make a difference. Use automation to simplify the process. Also, consider whether your 3-6-9 target needs adjusting to match any recent lifestyle changes – for instance, if you’ve had a baby, bought a new house or become self-employed.

When your emergency fund is “enough”

Your emergency fund is about peace of mind, not perfection. And once you’ve reached your target, you’re in the perfect place to redirect that savings habit toward other goals. For example, you might:

-

Focus on debt repayment

-

Save toward a home down payment

-

Aim for short-term goals such as a new car or a dream vacation

Common emergency fund mistakes to avoid

Before you get started, review these common errors many Canadians make when it comes to emergency funds:

Using your chequing account

If all your money is in one bucket, it’s too easy to accidentally spend your savings. Keeping your emergency fund in a separate account can help you save while still letting you easily access your money in case of an emergency. A savings account with a higher interest rate may help your emergency fund grow a little faster.

Saving too slowly

Your emergency fund target might feel challenging, but setting this money aside is important for your financial security. Review your budget and find ways to make those transfers as big as possible.

Dipping into your fund

You might be tempted to use your emergency fund for a splurge, but that’s not what it’s meant for. Keep it out of sight, add to it according to your plan and otherwise don’t think about it until you really need it.

Not rebuilding

When you go through tough financial times, survival mode kicks in, and it can be easy to forget about the future. But after the dust settles post-emergency, it’s important to rebuild your fund in case there’s a next time.

Emergency funds: An essential financial tool

An emergency fund is an important way to protect yourself against unexpected expenses while keeping your finances intact. Start building one today, and over time, you’ll have a safety net that will have you face a crisis without jeopardizing your financial future.

FAQ

Think of an emergency fund as a safety net for your finances so that if something unexpected happens, you won’t have to dip into savings or go into debt to cover it. It’s worth it to be prepared.

It’s a good idea for everyone who has expenses to have an emergency fund. While student emergencies might look like a broken laptop or an unexpected car repair rather than a mortgage payment, having a cushion may help them avoid going into debt to cover it. Plus, building the habit of setting aside small amounts early helps create long-term financial security.

That’s generally not recommended. You want to be able to access your emergency fund whenever you need it. Stock market values can fluctuate, and if the market is down when you have an emergency, you might be forced to sell your investments at a loss.

An emergency fund should be kept in a liquid, low-risk account, such as a high-interest savings account or a cashable GIC. The priority for this money is that it’s available when you need it, without the risk of losing its value.

While paying off high-interest debt is important, having even a small emergency fund can help you avoid taking on new debt when an unexpected expense arises. Organize your budget so you can build a basic cushion while also working on your debt repayment plan.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.