TLDR

The average Canadian university graduate with student debt owes more than $30,000.

Federal student loans are interest-free, but some provincial loans may still charge interest.

Federal loan repayments typically start six months after graduation.

Government assistance programs, such as the Repayment Assistance Plan (RAP) can help manage and reduce payments based on income.

Paying more than the minimum can reduce interest and shorten the repayment timeline.

Congrats! You’ve put in the hard work, tossed the cap and framed the diploma. Now you’re entering the working world, and it’s time to build a plan for your next milestone: repaying student debt. If you’re among the roughly 50% of Canadian graduates managing student loans, you need an easy-to-follow strategy to help you stay on top of your finances and avoid unnecessary stress.

Whether you’re paying back interest-free federal student loans or a private Student Line of Credit, this guide explains how to build a student loan repayment plan that fits your budget without sacrificing your future goals.

How much student debt do Canadians graduate with?

You’re not alone in managing the transition from graduation to loan repayment. Here’s what half of Canadian post-secondary graduates are navigating today:

Average student debt in Canada in 2026

According to the most recent data from Statistics Canada, the average bachelor’s degree graduate with student debt leaves school owing just over $30,000. This number varies, with balances sometimes exceeding $50,000 for professional programs such as medicine, dentistry and law.

Why repaying student debt feels harder today

Paying back student loans can feel more challenging today because graduates are entering a world of hefty expenses that are continually rising. The disposable income graduates once had available to pay off loans is now being spent on the rising costs of essentials such as groceries, rent and utilities.

In major cities like Vancouver, where an average one-bedroom apartment can cost close to $2,000 a month, student loan payments can be a significant burden. It’s also getting tougher to find a job. Youth unemployment rates are near record highs, according to Statistics Canada, making having a structured repayment plan even more important.

How does student loan repayment work in Canada?

Understanding how your debt is structured is the first step toward building an effective repayment plan.

Canada Student Loans vs. provincial loans vs. student lines of credit

Most Canadian graduates carry debt that’s a mix of government and private funds. Each has its own set of rules, rates and repayment requirements.

- Canada Student Loans (federal portion)

This is the foundation of most government aid. In 2023, the federal government eliminated interest on these loans. This is your most predictable debt because you only repay what you borrowed. Repayment typically begins six months after you finish your studies.

- Provincial loans (such as OSAP, the Ontario Student Assistance Program, or Alberta Student Aid)

Provincial loans are often integrated with federal loans through the National Student Loans Service Centre (NSLSC) but may still charge interest.

For example, most OSAP recipients have an Integrated Student Loan, combining federal and provincial student aid into a single loan. While the federal portion is interest-free, the Ontario portion may still charge interest (typically at prime +1%). Interest may also accrue during the six-month grace period.

- Student lines of credit (private loans)

These are private loans offered by banks and typically have variable interest rates tied to the bank’s prime rate. Unlike government loans, lines of credit usually require you to pay at least the monthly interest while you’re still in school. However, they offer more flexibility. You can borrow only what you need, and RBC typically offers a grace period of up to 24 months after graduation before you must begin repaying the principal.

When do you start repaying student loans in Canada?

- Federal loans: 6 months after you graduate.

- Provincial loans: Typically six to 12 months after graduation. Interest rates may be charged during this time.

- Private student lines of credit: Interest payments typically start immediately, and banks may offer a grace period of up to 24 months after graduation for principal repayment

Be sure to confirm your repayment schedule with your lender to avoid missed payments.

How to check your student loan balance and payment schedule

Most government loans are managed through the NSLSC, the official government of Canada repayment platform. Log in to your account to see your account balance, repayment start date, monthly amount and interest rates.

For private loans or bank lines of credit, log in to your bank account to review your balance and payment schedules.

What is the minimum payment on student loans in Canada?

When it’s time to start repaying your loan, your lender will use a certain formula to calculate your minimum monthly payment based on your loan balance, interest rate and repayment term (typically 114 months for government loans) to ensure you pay it off by a specific date.

While you must make the minimum payment, you can always pay more to reduce your balance faster and save on interest.

Understanding the interest on your student loans

- Federal loans: Interest-free

- Provincial loans: May charge interest depending on your province

- Private loans: Usually variable rates tied to prime.

Interest is the cost of borrowing money and if there’s an increase in the prime rate, while your monthly payments may remain the same, more of your payment will go towards interest meaning it will take you longer to pay off your loan.

What happens during the six-month grace period?

The six months following graduation are often referred to as a “grace period”, buying you some time to find a job and get financially settled. During this time:

- No payments are required on federal loans

- Interest does not accrue on federal loans

- Interest may accrue on provincial loans

While there is no formal grace period on private loans or lines of credit, your bank allow you to defer your principal repayment for up to 24 months. However, you will still be required to pay the monthly interest.

Student loan repayment options

Finding strategies that work for your lifestyle, income and financial goals is key to managing your payments. Whether it’s automating your contributions or finding new ways to boost your income, these steps can help you determine the best repayment plan for you.

| Repayment option | Who it is for | Key benefit |

|---|---|---|

| Standard plan | Stable income | Predictable payments over 114 months |

| Repayment Assistance Plan (RAP) | Lower income | Reduced or $0 payments |

| Extended term | High expenses | Lower monthly payments |

| Extra payments | Extra cash flow | Faster payoff, less interest |

| Student line of credit repayment | Variable income | Flexible repayment |

What is the Repayment Assistance Plan (RAP)?

The Repayment Assistance Plan (RAP) is a Government of Canada program that can reduce, pause or eliminate your monthly student loan payments based on your income. You can apply for RAP as soon as you start repaying your loan and must reapply every six months to remain eligible.

What happens if you miss a payment?

Missing a payment can impact your credit score for up to six years, which may make it harder to get approved for future loans (such as a car loan) or for an apartment lease.

After nine months of missed payments, the federal portion of your loan may be transferred to the Canada Revenue Agency (CRA) for collections, and you may lose access to future student aid.

If you think you might miss payment, reach out to your lender beforehand to explore your options.

Building a student debt repayment plan

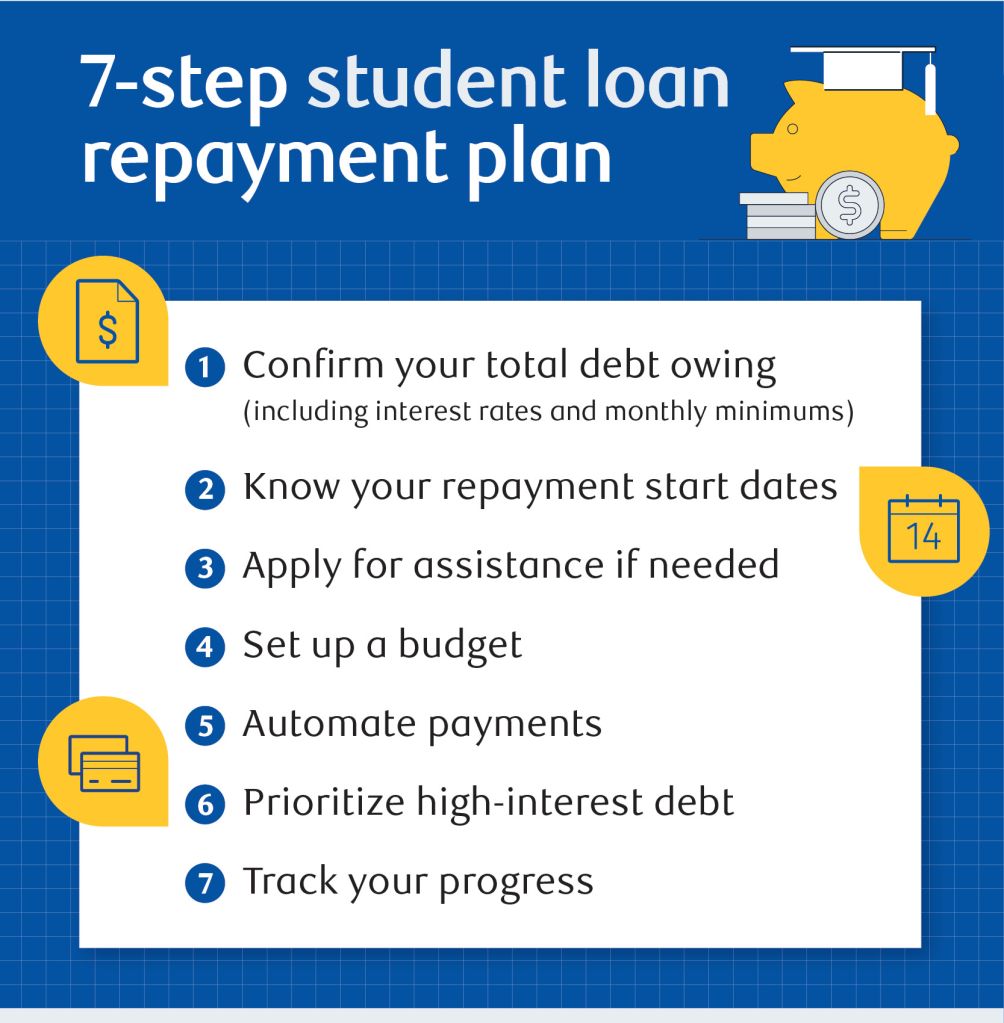

7-step student loan repayment plan

Before you start repaying your loan, follow these steps:

- Confirm your total debt owing, including interest rates and monthly minimums

- Know your repayment start dates

- Apply for assistance if needed

- Set up a budget

- Automate payments

- Prioritize high-interest debt

- Track your progress

How much should you pay toward student loans each month?

The minimum amount you’ll be required to pay each month is calculated using current interest rates, your principal balance and the maximum remaining term available to you. However, you can always pay more than the required amount, which will help your total interest and repayment time.

Automating student loan payments

Setting up pre-authorized automatic payments through the NSLSC means the minimum amount you owe will be electronically withdrawn from your bank account each month and put toward your loan. To set up automatic withdrawals, log in to your NSLSC online account, click My Account and select Pre-Authorized Debit. This will ensure that you never miss a payment and helps to protect your credit score.

Living with parents to pay off debt faster

While this isn’t a viable option for everyone, living with your parents after graduation could help you get ahead of your loan repayments. Paying nothing (or a minimal amount) for living costs lets you divert the money you would have spent on rent (which can cost $2,000 a month on average in Canada’s biggest cities) to your loan, helping you pay it down faster. For example, putting an extra $1,500 per month toward a $30,000 loan could help you become debt-free in under two years, saving thousands of dollars in interest.

Reducing debt with a side income or gig work

It can be tough for new graduates to find a full-time job, but taking on part-time or freelance work can help you earn a bit of extra cash to put toward your loan. Think about how you could turn your skills and passions into a side hustle. Maybe it’s mowing lawns in the summer or tutoring high school students.

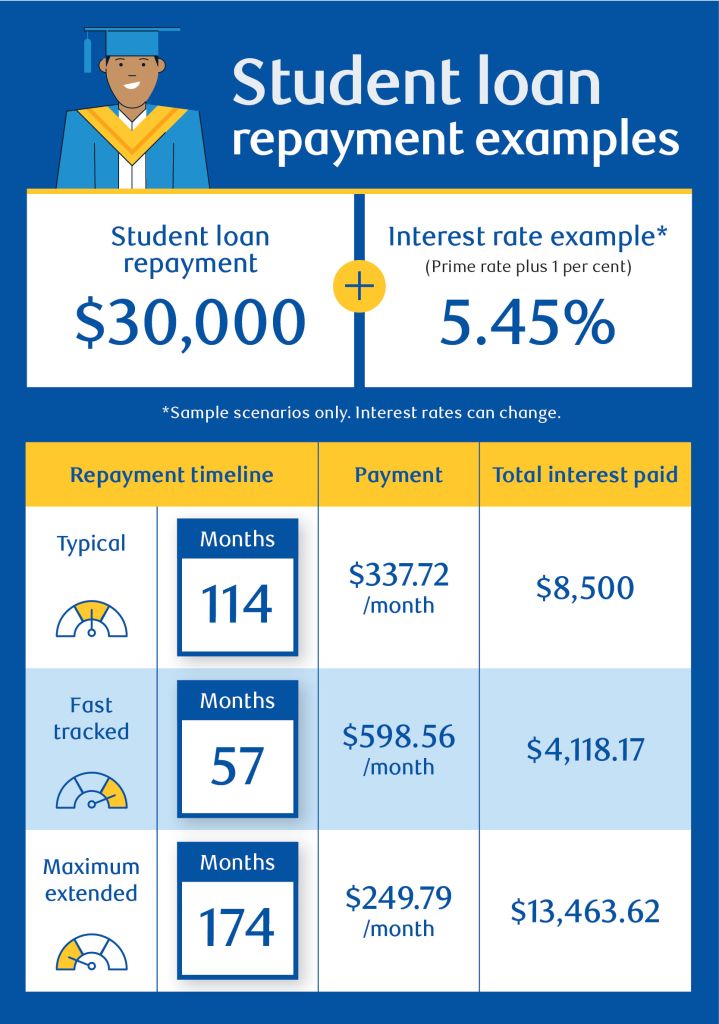

How long does it take to pay off student loans in Canada?

The typical maximum repayment period is 9.5 years (114 months) for government student loans in Canada. However, repayment timelines will vary based on your personal payment strategy, income growth and whether you make extra payments. You can also increase your monthly payment at any time to pay off your debt faster and save on interest. Here’s a look at how different scenarios can impact your schedule.

Example repayment timelines

Assuming a $30,000 loan at 5.45% (prime rate as of March 2026 +1 per cent):

- 114-months: $337.72/month, total interest of $8,500

- 57 months: $598/month, total interest of $4,118.17

- 174 months (maximum term): $249/month, total interest of $13,400

Source: Loan Repayment Estimator – CanLearn.ca

How extra payments can accelerate your timeline

Making lump-sum contributions in addition to your regular monthly instalments can lower your total interest owed and help you pay off your loan faster. You can make these extra payments at any time. An extra $100 per month on a typical $30,000 loan can reduce your repayment period by about two years and reduce total interest paid by $3,500.

What happens if you only make minimum payments?

There is no penalty for making only the minimum payments, but if you make additional contributions, you can pay off the loan sooner.

How salary growth changes repayment timelines

When you first graduate, you may earn an entry-level salary that only allows you to make the minimum monthly payment. But as your income grows, consider allocating the extra money toward your loan to pay it off faster.

Balancing student loan payments with financial goals

Repaying your loans doesn’t mean you can’t build your savings with the right strategy.

Pay high-interest debt before student loans

If you have higher-interest debt, such as credit cards, you may consider paying these off first. While you will still need to make the minimum payment on your student loan to avoid penalties, any extra cash you have can go toward higher-interest debt first.

Prioritize building an emergency fund

Depending on your situation, you may want to focus on building up a cash reserve for financial emergencies that could derail your repayment plan if you have no funds set aside. For instance, maybe you drive a car to work and want to keep money on hand in case it breaks down and needs immediate repair.

Can you invest in a Tax-Free Savings Account (TFSA) while repaying loans?

Yes, you can invest in a TFSA, but it’s important to weigh the risks. If the interest rate on your loan is higher than what you expect to earn in the market, you may want to consider putting your extra cash toward the loan first.

Student loan repayment vs. saving for a home

You can still save through a TFSA or First Home Savings Account (FHSA) while paying down your student debt. How much you save versus how much you put toward your loan will depend on your specific situation and timeline.

What if you can’t afford your student loan repayments?

Life can be unpredictable, but your student loan doesn’t have to be a source of stress. There are programs designed to help keep your repayment plan manageable. You should seek assistance if:

- You’re unemployed or working reduced hours

- Your income is below the RAP threshold for your family size

- You’re struggling to afford minimum payments

- You’ve missed or are about to miss a payment

- Other debts are overwhelming your budget

Repayment Assistance Plan (RAP): How it works

The Repayment Assistance Plan (RAP) can reduce, pause or eliminate your monthly student loan payments based on your income and requires reapplication every six months to remain eligible.

How RAP lowers or pauses payments

- Payments may be reduced to $0

- Government may cover unpaid interest

- After extended use, part of the principal may be repaid by the government

When to talk to a financial advisor

If you are struggling to make your student loan payments and feeling overwhelmed, it may be time to talk to a financial advisor. They can help you create a debt management plan and direct you to more specific services, such as credit counselling.

How credit counselling works in Canada

Credit counsellors can offer a range of services, including debt repayment plans, one-on-one counselling and seminars. One way to find an accredited credit counselling agency is through Credit Counselling Canada. However, it’s important to do your research before working with an agency to avoid being misled. Watch for unrealistic promises (like fixing your credit score overnight).

FAQs

Paying off your loans early will reduce the total interest you owe, freeing money up for savings goals like buying a house. But your ability to do so, depends on your financial goals and timelines.

Minimum payments are based on your loan balance, interest rate, and repayment term (typically 114 months for government loans)

You can’t deduct the principal amount of your student loan. However, you may receive a 15 % tax credit on any interest you pay on your government student loans each year.

Yes, your student debt affects your ability to qualify for a mortgage in Canada. Your student debt affects your total debt service ratio, which is the gross annual income required to cover all debt payments, such as your house, credit cards and student and personal loans. When you apply for a mortgage, your lender will factor in your monthly student loan payments. A $400 monthly obligation can significantly reduce your borrowing power.

Missing a single loan payment can hurt your credit score. If you miss nine consecutive payments, the federal portion of your loan is referred to the CRA for collection. At that point, you won’t have access to further student aid. You can contact the CRA to help you set up a repayment plan to get the federal portion of your loan back in good standing. You can also contact your province or territory to help with the provincial or territorial portion of the loan.

The federal government offers Canada Student Loan Forgiveness to borrowers in certain essential professions (such as teachers, family doctors and dentists) and in eligible communities, such as rural areas or places with a population of 30,000 or less. Loan forgiveness can only be applied to the outstanding part of your federal student loan. However, your province or territory may also offer loan forgiveness.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.