TLDR

Post-secondary education in Canada can exceed $30,000 per year when tuition, rent, food, transportation and books are factored in

Starting early with a Registered Education Savings Plan (RESP) allows for tax-deferred growth and unlocks valuable government grants like the Canada Education Savings Grant (CESG) and Canada Learning Bond (CLB)

Families can bridge savings gaps through scholarships, bursaries, government student aid, loans and shared cost arrangements

Aside from the rising cost of living and inflation, post-secondary expenses have soared in recent years. As a parent, tuition, transportation, books and living arrangements are just a few of the factors to consider when planning for your child’s education. While it may seem like a significant financial obligation, there are ways to manage these costs.

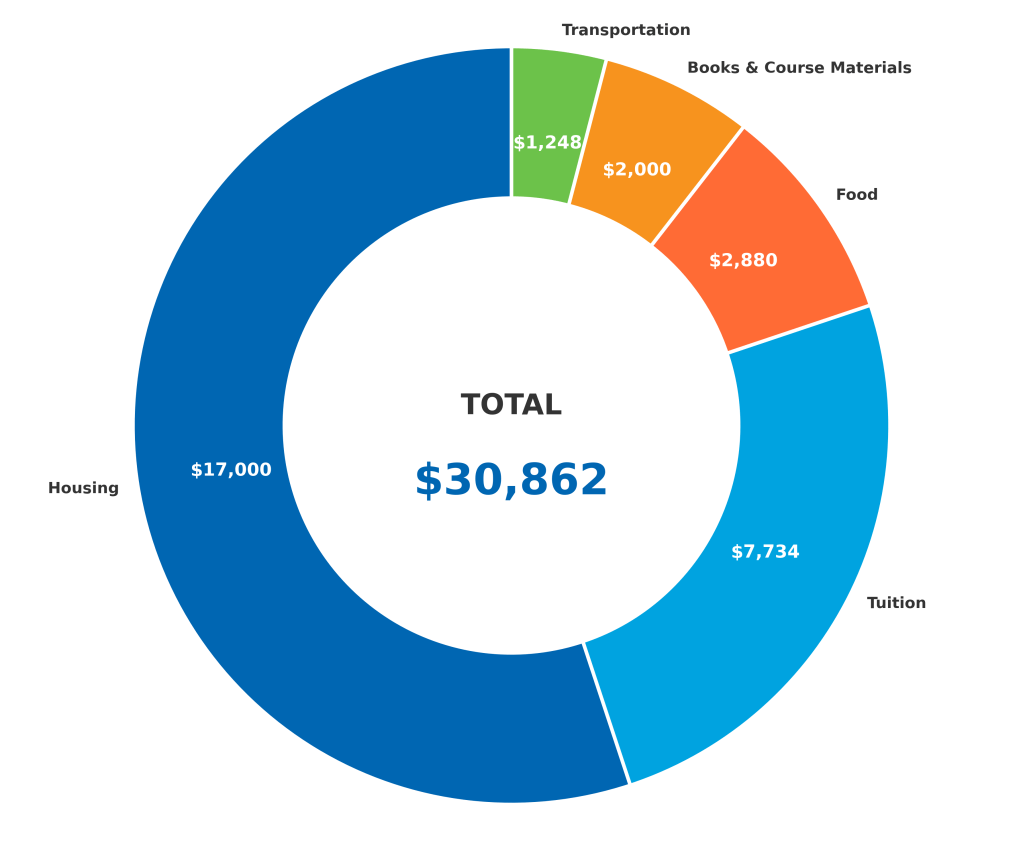

How much does university cost in Canada per year?

The total cost of post-secondary education in Canada can vary widely depending on the school, program and whether a student lives at home.

Tuition

According to Statistics Canada, post-secondary annual tuition costs for undergrads are expected to reach $7,734 in the 2025/2026 academic year – a 1.4% increase from the previous year. Graduate tuition is expected to average $7,978 – up 0.9%. Tuition costs can vary by program and represent only part of the total cost.

Housing costs

According to a Studenthaus study of 6,000 Canadian students, those students living away from home pay an average of $1,146 per month for rent. In major cities like Toronto, average rents can range between $1,600 and $1,800 per month, depending on location and housing type. In many cases, student leases are signed for 12 months, meaning students may pay rent year-round even though they only live in the unit during the academic year (typically 8 months) depending on the housing arrangement.

Food

According to EduCanada, students can expect to spend approximately $240 to $480 per month on groceries and dining out, depending on lifestyle and location.

Transportation

Transportation costs can also balloon to a high cost whether the student owns a car or takes public transport. EduCanada estimates that a monthly public transit pass can cost up to $156 per month, depending on the city. This doesn’t include train or plane tickets home for the weekends or holidays.

Books and course materials

Textbook and academic supplies can also add up. The University of Toronto advises students to budget $1,000 and $2,000 per year depending on program needs.

Additional expenses can include:

- Utilities such as hydro and internet

- Tenant insurance

- Phone service

- Personal expenses and entertainment

When all these costs are combined, the total annual cost of attending university in Canada can exceed $30,000 per year, particularly for students living away from home.

Average annual cost of post-secondary education in Canada

*Sources: Statistics Canada, EduCanada, Studenthaus, University of Toronto

How much should parents save?

The exact amount parents should save will vary depending on the financial circumstances of the family and the type of program chosen.

Rough estimates put the annual cost of post-secondary education at $30,000 – meaning a four-year program in Canada could cost over $100,000. These estimates are based on 2026 costs, but education expenses can change over time, including during the years spent in post-secondary education.

This doesn’t mean parents need to save the entire amount on their own. Consistent RESP contributions – for example $100 a month from birth – can snowball into a large education fund over time, especially when combined with government grants like the Canadian Education Savings Grant (CESG).

-

Contributing $100 per month adds up to $21,600 in contributions, and when combined with the minimum CESG grant of $4,320 (based on a 20% match) and modest investment growth, total savings could exceed $40,000.

-

The average monthly RESP contribution is approximately $153 (based on 2024 data from the Government of Canada) which tallies up to $1,840 each year. This would generate an additional $368 per year in CESG grants.

-

Contributing $2,500 annually into an RESP allows families to benefit from the maximum annual CESG amount of $500 per year, up to a lifetime maximum of $7,200 per child.

-

A one-time $50,000 RESP contribution made at birth could grow to approximately $120,000 by age 18, assuming a 5% average annual return. Under the current rules, only the first $2,500 contributed per year is eligible for the CESG, meaning a lump sum contribution would typically result in a single year of grant eligibility (approximately $500) with the remainder of the contribution receiving no additional matching grants. While this approach means foregoing additional CESG that could have been earned over time, contributing earlier allows for a long period of investment growth, which may help offset some of the trade-off.

How regular monthly contributions grow over time

This table shows the projected value of RESP savings at age 18, based on different monthly contribution amounts and starting ages. Calculations include the 20% Canadian Education Savings Grant (CESG) on eligible contributions and assume a conservative 5% average annual return.

$50/month

| Starting at Birth | Starting at Age 5 | Starting at Age 10 | Starting at Age 15 | |

|---|---|---|---|---|

| Your contributions | $10,800 | $7,800 | $4,800 | $1,800 |

| CESG grants | $2,160 | $1,560 | $960 | $360 |

| Projected total at 18 * | $20,900 | $13,100 | $7,100 | $2,300 |

*Projected totals include contributions, CESG grants, and estimated investment growth at 5% average annual return. For illustration purposes only, actual returns will vary.

$100/month

| Starting at Birth | Starting at Age 5 | Starting at Age 10 | Starting at Age 15 | |

|---|---|---|---|---|

| Your contributions | $21,600 | $15,600 | $9,600 | $3,600 |

| CESG grants | $4,320 | $3,120 | $1,920 | $720 |

| Projected total at 18 * | $41,800 | $26,300 | $14,100 | $4,600 |

*Projected totals include contributions, CESG grants, and estimated investment growth at 5% average annual return. For illustration purposes only, actual returns will vary.

$150/month

| Starting at Birth | Starting at Age 5 | Starting at Age 10 | Starting at Age 15 | |

|---|---|---|---|---|

| Your contributions | $32,400 | $23,400 | $14,400 | $5,400 |

| CESG grants | $6,480 | $4,680 | $2,880 | $1,080 |

| Projected total at 18 * | $62,700 | $39,400 | $21,200 | $7,000 |

*Projected totals include contributions, CESG grants, and estimated investment growth at 5% average annual return. For illustration purposes only, actual returns will vary.

$208/month

| Starting at Birth | Starting at Age 5 | Starting at Age 10 | Starting at Age 15 | |

|---|---|---|---|---|

| Your contributions | $44,928 | $32,448 | $19,968 | $7,488 |

| CESG grants | $7,200 | $6,490 | $3,994 | $1,498 |

| Projected total at 18 * | $84,800 | $54,600 | $29,400 | $9,700 |

*Projected totals include contributions, CESG grants, and estimated investment growth at 5% average annual return. For illustration purposes only, actual returns will vary.

How to save for a child’s post-secondary education

For many families, investing in a Registered Education Saving Plan (RESP) offers tax-deferred growth and access to government grants. Speaking with a financial advisor can help families learn how to maximize the financial potential based on their goals.

What is an RESP and how does it work?

A Registered Education Savings Plan (RESP) is a tax-deferred savings plan designed to help save for a child’s post-secondary education.

RESP funds can be used for eligible education programs including:

- Universities and colleges

- CEGEP programs

- Trade schools

- Apprenticeships

Parents, grandparents and loved ones can contribute to the RESP over the years and since contributions grow tax-deferred, investment earnings compound until the funds are withdrawn for education expenses.

Canada Education Savings Grant (CESG) and Canada Learning Bond (CLB)

The Government of Canada provides incentives to help families save for education.

-

The Canada Education Savings Grant (CESG). The government matches 20% of annual RESP contributions up to $500 per year with a $7,200 lifetime maximum per child

-

The Canada Learning Bond (CLB) This bond provides an additional $2,000 for eligible low-income families, with no requirement for personal contributions to be made. It includes an initial payment of $500 and then $100 for each year of eligibility, up to the age of 15 – for a maximum of $2,000.

What if savings don’t cover the full amount?

Even while saving diligently, some families may face a funding gap. If RESP savings do not fully cover education costs, students can look to the following to help finances the remaining expenses:

- Scholarships

- Bursaries

- Government Student Loans

- Student loans

- Student Lines of Credit

Understanding these options early can help families make informed financial decisions before a student starts their education journey and reduce the reliance on higher-interest borrowing.

Even after maximizing RESP and CESG contributions, there may still be a shortfall, leading some to supplement savings with flexible TFSAs or non-registered accounts. While individual circumstances vary, consistent RESP contributions remain a meaningful savings step for many households.

Scholarships and bursaries

Scholarships and bursaries are forms of non-repayable financial aid.

-

A scholarship: these funds are typically awarded by governments, schools or private organiztions and are based on:

- Academic achievement

- Athletic skill

- Community involvement

-

A bursary: these are awarded based on financial circumstances, usually to a student who has proven to be unable to afford to pay for tuition fees.

A student should be looking into bursaries and scholarships as soon as their senior grade begins. Guidance counsellors and department heads are a great resource and can help with identifying relevant opportunities. They will know what’s available and which scholarships receive the least number of applicants. A student can also start their research by looking at their target university’s financial aid website.

Students can also search for opportunities on the Scholarships Canada website, which provides customized scholarship matches tailored to their specific field of study, academic average and extracurricular activities.

Student loans and Government assistance

The government and financial institutions offer student loan programs with different terms and conditions depending on the student’s financial situation and program needs.

-

Government student loans are typically based on financial circumstances, and often require students to maintain a minimum course load and academic average. Eligibility is typically based on:

- Household income

- Family size

- Enrollment status

-

Enrollment statusThe Canada Student Financial Assistance Program provides federal grants and loans and alongside provincial aid programs such as the Ontario Student Assistance Program

-

Student lines of credit, offered by financial institutions, provide flexible loans to cover tuition and living expenses. These products often allow:

- Interest-only payments while studying

- Flexible repayment options after graduation

- Additional payments without penalty

For more information, here is a comprehensive breakdown of student loans in Canada.

Who pays for what? Finding family balance

Post-secondary education is often a shared financial responsibility between parents and children. Every family situation is different but three common scenarios exist:

Scenario Parent Contribution Student Contribution Pros Cons Parents cover majority of costs Full tuition + living costs Minimal (personal expenses) Less financial stress on student, student can focus on academics High cost for parents, may impact retirement savings Shared costs (agreed split) Partial tuition or matching contributions Part-time work, personal savings Encourages financial responsibility, shared burden Requires a clear agreement, may cause tension if student or parent are unable to meet obligations Student primarily responsible Minimal support Tuition, living costs, work, scholarships, loans Student gains independence and money management skills High stress on student, risk of high debt if not well planned Open communication about finances can help families set realistic expectations and reduce stress during the transition to post-secondary education.

When to start saving and planning for university costs

Parents can open and start contributing to an RESP as soon as their child is born and has a Social Insurance Number (SIN). Starting early will give access to:

- up to 18 years of tax-deferred investment growth

- Government grants such as the CESG and CLB

- A maximum lifetime contribution limit of $50,000 per child

The child has up to 35 years to use the funds, offering flexibility should they decide to delay their education.

How to balance education savings with your own financial future

Careful management of savings and RESP could do most of the heavy lifting, but saving for a child’s education should not come at the expense of the parents own long-term financial security. Parents should be sure to:

- Continue contributing to retirement savings while saving into an RESP

- Avoid excessive debt to meet ‘expectations’

- Set realistic contribution expectations

Involving teens in the financial planning conversations can help them become savvy when it comes to money management and ultimately less stressed when it comes to their own finances. Tools such as the RBC Student Budget Calculator and the Government of Canada website, can provide a clearer vision of post-secondary needs, expenses and availability of financial support.

Is post-secondary education worth the cost?

Post-secondary education can open doors to career opportunities, skill development and personal growth, but its financial value varies widely depending on the program, field of study and total costs. Evaluating program options carefully can make a significant difference. Families may benefit from asking questions such as:

- What career paths are linked to this program?

- How long will it take to complete?

- Are there alternative pathways like college diplomas or trade apprenticeships?

Making informed decisions ensures that the education investment matches both the student’s ambitions and the family’s financial reality.

FAQ

The average undergraduate tuition in Canada is about $7,734 per year. The inclusion of transportation, rent, food and books can bring the overall total annual cost to $30,000, with many variables to consider.

While there’s no one-size-fits-all answer for this, many parents will aim to save between $25,000 and $50,000 per child through RESP contributions with government grants and investment growth to helping to increase the total savings over time.

Scholarships, bursaries, government student aid programs, loans and student lines of credit can go a long way in closing financial gaps, no matter how big they are. Gaining an early understanding of the funding sources available can help reduce the reliance on higher-interest debt once the child starts their university education.

This decision should be based on financial ability rather than obligation. A parent wouldn’t want to endanger their retirement plans while also not leaving their children without any help. In light of this, many families encourage their children to share the financial responsibility by seeking out jobs, scholarships or student loans.

Families can start saving as soon as the child has a Social Insurance Number, maximizing access to government grants and allowing for tax-deferred, compounded growth on savings.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.