Climate change is one of the most pressing issues worldwide and many countries, including Canada, have set ambitious targets to reduce greenhouse gas emissions (GHGs) to net-zero in 2050.

Achieving net-zero — when GHGs going into the atmosphere are balanced by removal out of the atmosphere — will lead to major changes in how Canadians live and do business. It will also require huge investments in game-changing technologies, like carbon sequestration and storage, to build the infrastructure required to support a low-carbon economy – everything from electric vehicles to renewable energy sources.

Still, the risk of doing nothing, or not enough, may have a devastating impact on the environment and the economy. Canadians only need to look as far as British Columbia, which has become an example of the diversity of issues climate change is already causing.

In late 2021, British Columbia experienced devastating floods, caused by record rainfall over two days. The floods came only months after the province saw a record-breaking heatwave and devastating forest fires. The severe weather events damaged infrastructure, homes and businesses while also cutting off road and rail links, halting the international exchange of goods.

Canada’s climate playbook

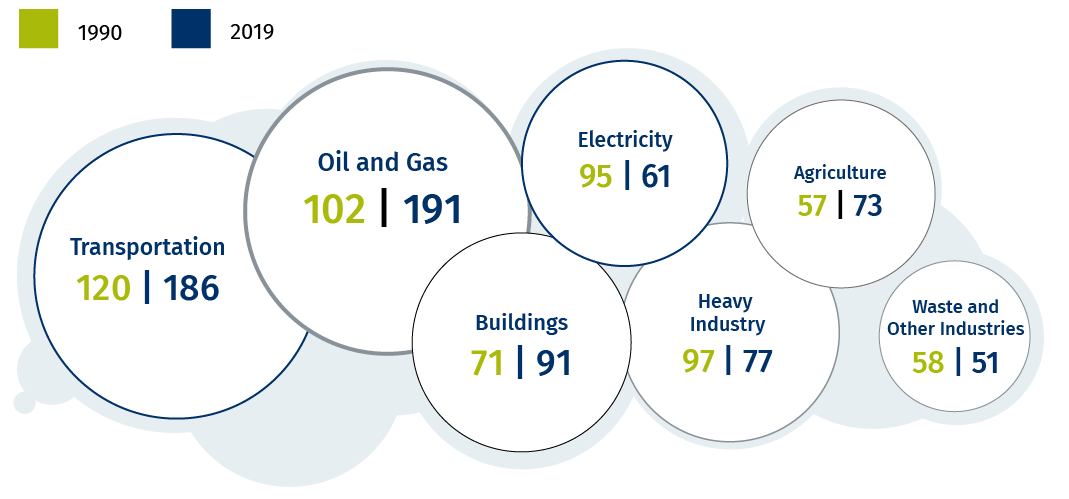

While emissions rose in several sectors from 1990 to 2019, Canada’s goal is to cut emissions by 40 per cent by the end of this decade and to reach net-zero by 2050.

Canadian Emissions by Sector

Source: Environment and Climate Change Canada, RBC Economics

Units: Greenhouse gas emissions, million tonnes of CO2 equivalent

“At this point, we are behind,” RBC president and chief executive officer David McKay stated in an article in The Globe and Mail.

“We are not tackling climate change fast enough to succeed. And we need to make the biggest economic transition of our lifetime in an orderly fashion, so we create prosperity for Canadians rather than destroy industries and sectors that Canada relies upon,” McKay wrote. “Business as usual won’t get us there. It will take a new playbook to increase and scale climate activities and investments faster.”

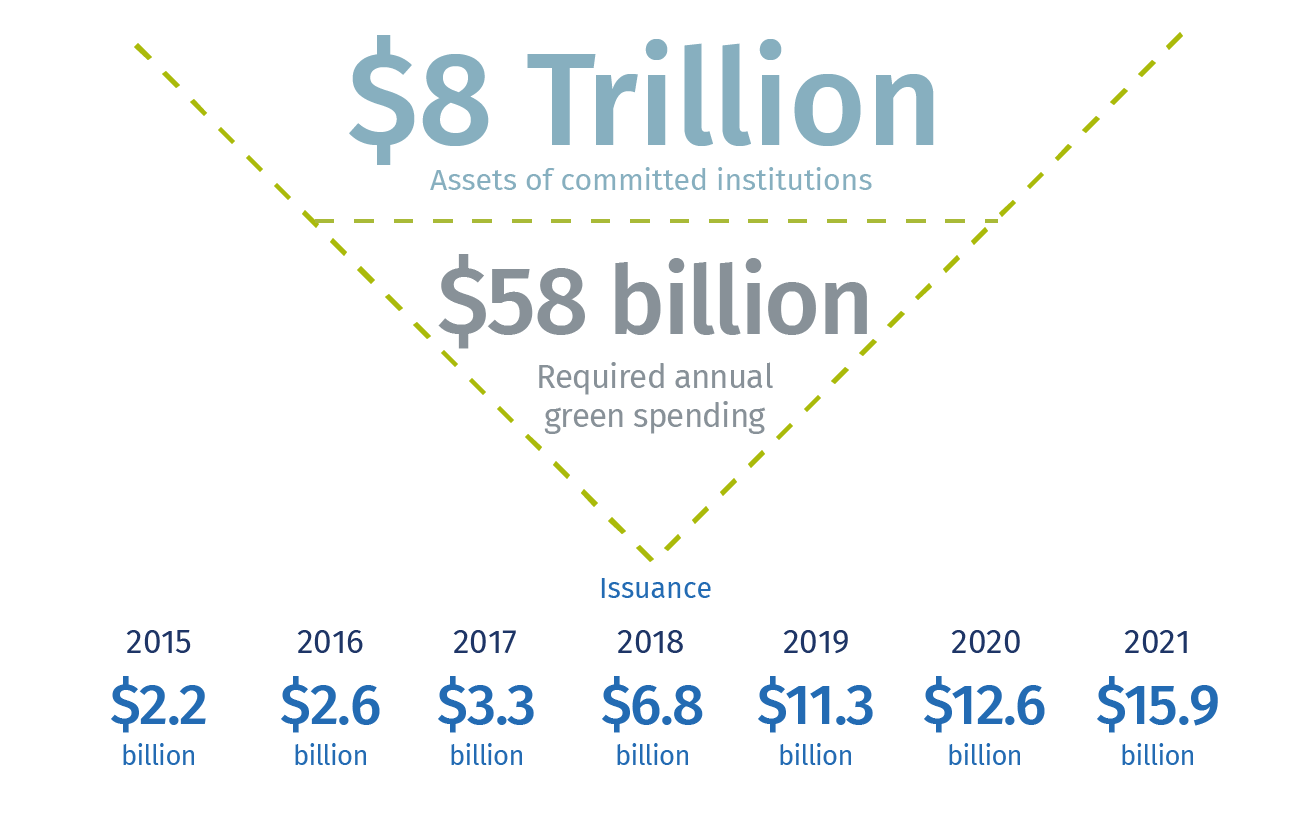

An RBC Economics report shows Canada would need to spend about $2-trillion in the next three decades to increase and scale climate activities and investments. That’s about $60-billion annually to cut the country’s emissions by 75 per cent from current levels, which is about as far as Canada can get with current technologies, the report states, and up from about $15-billion today.

Required Annual Green Spending

Source: Bloomberg, RBC Economics; *data to 1 November 2021

“The ambition to achieve net-zero should be seen as an opportunity to transform every sector of our economy,” says Sue Noble, Vice President, Commercial Financial Services Strategy at RBC. “We have seen a lot of change already across companies and industries and we will see much more in the years to come.”

How business owners can adapt to net-zero goals

The pace of change for companies will depend on the organization, its operations, and the industry it’s in, Noble says.

Businesses should start to think about how green pathways can become embedded in their corporate growth strategy, purpose and values.

To be successful, Noble says companies shouldn’t try to go it alone but seek the knowledge, advice and support of like-minded organizations and other stakeholders, including investors and employees, who are also concerned about the impacts of climate change.

“People and organizations increasingly want to work for, invest in and do business with companies whose values are aligned with theirs,” Noble says.

Numerous studies also show there’s a strong investment case for being more sustainable, including reducing costs and operational risk.

Former Bank of England and Bank of Canada Governor Mark Carney has said the transition to net-zero “is creating the greatest commercial opportunity of our age,” according to a Bloomberg report from November 2020.

Making the sustainability investment upfront “will help drive business efficiencies and yield returns over the long term,” Noble says, adding that doing nothing could also put the companies at a competitive disadvantage.

While there is no universally adopted set of guidelines for companies looking to improve their sustainability performance, there are many companies and organizations that can provide advice. For example, a large company could look to the Task Force on Climate-related Financial Disclosures (TCFD) framework and their MSCI ratings, whereas a smaller business could look into becoming a certified B Corp., which is a designation that a business is meeting high standards of verified performance, accountability, and transparency on various factors.

Noble recommends business owners and managers stay connected to various stakeholders and understand what initiatives might work best for their business.

“There’s not one business case or solution for every business,” she says. “Every industry is unique.”

For instance, some large retailers are choosing to pursue greater energy efficiency by upgrading refrigeration, lighting, and HVAC systems, while others have made the supply chain a greater priority by employing greater use of recycled and sustainably sourced materials.

Steps your company can take to improve sustainability

It’s never too early to start or strengthen sustainability measures in a business, Noble says.

She encourages companies to start by measuring their emissions. While this may be challenging for some businesses, Noble says knowing where your emissions are coming from is critical to effective abatement strategies.

Businesses could start as simply as auditing fuel use and then expand to electricity and then to broader emissions such as business travel, she says.

With that baseline, Noble says businesses should develop short- and long-term plans that include small steps at first and then progresses into broader changes.

“Start thinking about your own sustainability priorities,” she says. “What actions are you considering? What would have to be in place before you take those actions? What information are you missing?”

From there, companies can consider how to build and embed these changes into their corporate structure.

Business owners and managers should then talk to their customers, partners and suppliers about their plans and the ways in which they can work together to make meaningful changes.

“It’s an ongoing dialogue and a learning journey for everybody,” Noble says. “It’s recommended that business owners and managers make sustainability a regular part of conversations with their large customers and suppliers, understand their priorities, identify opportunities to share costs of sustainability improvements, provide recognition.” This step is particularly important as companies may start to be impacted by the targets and ambitions that their buyers or suppliers have set.

Business owners should also seek to understand the sustainability trends that are occurring within their own industries and aim to better understand what those trends will mean for the success of their business

RBC as a climate partner

RBC has set its own net-zero targets and investments as part of its Climate Blueprint and has partnered with several companies and organizations to help drive broader change.

In early 2021, RBC increased its commitment to mobilize $500-billion in sustainable finance by 2025. RBC’s initial commitment of $100-billion in sustainable financing was achieved in 2020.

It has also committed to net-zero emissions in its lending by 2050, aligned with the global goals of the Paris Agreement and to achieve net-zero emissions in its global operations annually: reducing greenhouse gas (GHG) emissions by 70 per cent and sourcing 100 per cent of its electricity from renewable and non-emitting sources both by 2025.

Noble says RBC is also proactively working with companies and organizations on how to best transition to net-zero.

“We believe that we can help our clients by leveraging our scale, information and connections to help our clients in their journeys and ultimately become a trusted climate partner to our clients.”

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.

Share This Article