TLDR

Seen as a last resort, bankruptcy can affect your credit score for up to seven years and may require you to give up some of your assets

Signs of impending bankruptcy can include missing scheduled payments, heavy reliance on credit and high debt levels

You may avoid bankruptcy by budgeting, reducing debt and by asking for help before things become unmanageable

Debt consolidation and consumer proposals are good alternatives to bankruptcy.

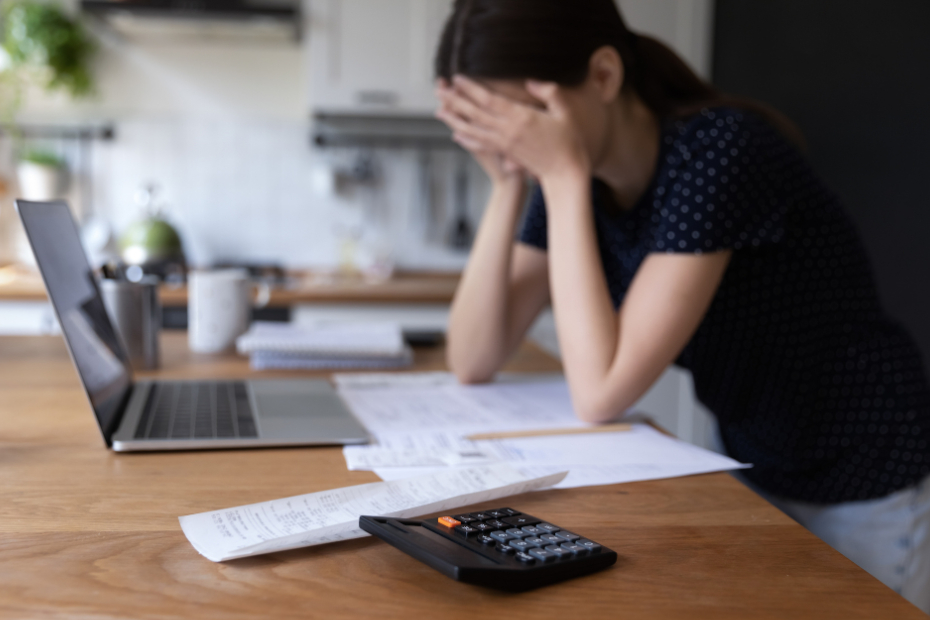

Financial stress can feel overwhelming, especially if you’re experiencing the keys signs of impending bankruptcy. But no matter how bad your personal finances might seem, there are strategies and alternatives to show you how to avoid bankruptcy in Canada.

Bankruptcy in Canada is a legal process under the Bankruptcy and Insolvency Act that eliminates most unsecured debt but can have an impact on your assets and ability to secure credit in the future.

Whether you’re dealing with out-of-control credit card debt, struggling with mortgage and car loan payments, or facing collection calls, there are credible options to help make ends meet. One of the first steps to turning things around is to recognize the signs of financial difficulty while you still have time to do something about it.

Many Canadians don’t realize they’re at risk of bankruptcy until their options feel limited, but acting early can open up more flexible and manageable solutions.

Signs you may be heading toward bankruptcy

If you’re constantly putting off paying for things when bills are due, juggling various sources of credit to expand your purchasing powers or relying wholly on credit to get by, you may be headed for trouble. Recognizing these signs early can help you get back on track before debt becomes unmanageable.

Using credit for everyday essentials

Using your credit cardas a sort of limitless ‘I owe you’ is doing more harm than good by increasing your balance, adding interest and possibly fees and penalties to what you now already owe.

Only making minimum payments on debt balances

Minimum payments mainly cover interest, making it difficult to reduce your overall balance. Paying the very least you can against your credit card balance might buy you time, but it won’t do much to save you money or eliminate your debt longer-term.

Missing mortgage or rent payments

Being delinquent with rent or mortgage payments will attract negative attention from creditors and negatively impact your credit score, directly affecting your ability to borrow more money. This won’t only affect your credit but could prove particularly challenging when you’re trying to rent a home or renew a mortgage in the future.

Taking payday or high-interest loans or borrowing from family

Payday or high-interest loans, as well as borrowing money from family, are all recipes for disaster. Payday loans can help you cover immediate, unexpected expenses until your next paycheque arrives. Unfortunately, fees can be quite high, and full repayment is typically expected on your next payday. Borrowing money from family can lead to all sorts of complications, especially when it comes to repayment terms, schedules and obligations.

Ignoring CRA or collection letters / feeling anxious opening bills

Avoiding opening bills and ignoring CRA or collections letters can make it harder to resolve your situation since creditors are less likely to want to deal with a delinquent borrower.

Debt payments exceeding 40% of income

If you’re spending close to half of your income repaying loans or credit it may signal that your debt is becoming unmanageable and there’s a good chance that you’re heading toward bankruptcy. Try to reduce spending and consolidate your debt in such a way that you’re not spending most of your repayments covering interest alone. Make sure that you’re able to make sizeable payments toward paying down the principal.

No emergency savings or using RRSP withdrawals to pay debt

A lack of savings can make it harder to manage unexpected expenses without relying on credit. Do your best to establish emergency savings and avoid relying on your RRSPs as a source of income to pay back your debt. Borrowing from your RRSP before its intended time could result in you losing some or all its intended tax benefits.

Why Canadians file for bankruptcy

Filing for bankruptcy is not an easy choice to make and is often influenced by some of the following factors:

- Job loss or income disruption

- Mortgage renewal payment shock or increases in rent

- Inability to keep up with increases in cost of living

- Divorce or illness

- High-interest debt accumulation

- Lack of emergency savings

What to do if you’re worried about bankruptcy today?

If you’re worried about going broke, stop using credit immediately. Contact your creditors before missing any payments and try to set up more manageable repayment terms. Acting early is important, as falling behind on bills can limit your options and may increase costs over time.

Check your credit report regularly to monitor your credit score and prioritize funds for essentials like housing, groceries and utilities. Speaking to a Licensed Insolvency Trustee (LIT) – the only professionals authorized by the federal government – can help you understand your options.

A step-by-step guide: how to avoid bankruptcy

There are several meaningful steps that you can take before considering bankruptcy — from reducing your personal spending to seeking out professional advice.

Step 1: Stop taking on new debt

Avoid using credit for everyday expenses as this can quickly increase your debt. If possible, pause borrowing and switch to cash or debit for daily spending. This can help you focus on paying down what you already owe.

Step 2: List all debt and interest rates – understand exactly what you owe

List all your debt along with balances, interest rates and minimum payments. This will give you a clear picture of what you owe and help identify high-interest debt.

Step 3: Minimize high-interest debt

Focus on reducing high-interest debt first to lower overall borrowing cost. This will help make debt repayment more manageable and ensure that you can make more reasonable contributions towards paying down the principal of the loan.

Step 4: Create a realistic, updated budget

Build a budget that truly reflects your current financial state: income, expenses and upcoming costs. Account for this when tracking your expenses and forecasting regular and upcoming costs.

Step 5: Live within your means (avoid lifestyle creep – possible link to article on lifestyle creep)

One of the best ways to manage your budget and not break the bank is to avoid spending what you don’t have. Live within or below your means and avoid lifestyle creep. This way, you’ll still be able to meet your financial obligations should some of your regular expenses suddenly go up.

Step 6: Contact your creditors

Reach out early to ask about payment flexibility or hardship options before you miss a payment

Step 7: Seek professional advice early – a credit counsellor or bank advisor

Don’t be afraid to seek professional help and to do so early in your financial journey. Credit counsellors and bank advisors can help you understand your options and the next steps.

Step 8: Build an emergency fund

Plan for the unexpected by building an emergency fund that can cover you for betwen three to nine months’ of expenses. You can place these emergency funds in a savings account, so that your money can accrue interest and in a fund separate from the one you use for your daily expenses.

Alternatives to Bankruptcy in Canada

Contrary to popular belief, there are several sound financial alternatives to declaring bankruptcy that may help you manage debt without declaring bankruptcy.

Consumer proposal

You may be able to work with a Licensed Insolvency Trustee (LIT) to create a consumer proposal, if you owe less than $250,000 in unsecured debt and your creditor(s) agree. LITs are regulated by the federal government through the Office of the Superintendent of Bankruptcy (OSB) under the Bankruptcy and Insolvency Act. They are the only professionals in Canada authorized to administer bankruptcies and consumer proposals.

Your LIT will work with you and your lenders to repay your debts over time. Just note that a consumer proposal typically lasts up to 5 years and will stay on your credit profile for the length of the agreement plus a year or two after completion, depending on your home province or territory and the credit bureau.

Debt consolidation

Consult aprofessional credit counsellor to advise you on a consolidated repayment plan, which combine your debts into a single, manageable payment, potentially reducing interest. Your counsellor will negotiate with your lenders on your behalf and seeking their services won’t negatively impact your credit score.

Credit counselling

Non-profit credit counselling can provide free financial assessments and personalized debt relief alternatives. It can also help with course-correcting financial paths without the need to involve the courts or government agencies.

Negotiating with creditors

You might be able to arrange more management repayment terms by reaching out directly to your creditors to discuss your situation. Please note that if the account has already gone to collections, it will appear and stay on your credit report and will impact your credit score.

Increase financial literacy

There are plenty of trusted and informative Canadian federal government resources that will allow you to better understand your options and obligations.

FAQ

To avoid bankruptcy, understand your finances, reduce expenses and avoid new debt. Contract creditors early and explore debt relief options such a debt consolidation or a consumer proposal. Speaking with a Licensed Insolvency Trustee or credit counsellor can help clarify your options.

Common signs of bankruptcy include relying on credit for everyday expenses, missing bill payments, carrying high-interest debt and spending a large portion of your income on debt repayment. Recognizing and acting on these signs early can help you act before debt becomes unmanageable.

You may be able to keep your house, depending on your home equity situation, your provincial or territorial exemptions and the debt solution you chose.

Yes, a consumer proposal is the most popular alternative to declaring bankruptcy. It can help you keep your house, regardless of the equity, while enabling you to repay a portion of your debt based on what you can afford and what your creditors agree to.

When debt starts to feel overwhelming and you’re having trouble making minimum payments or relying on credit, it’s time to chat with a LIT. Early support can help you explore alternatives like debt consolidation or a consumer proposal before bankruptcy becomes necessary.

This article is intended as general information only and is not to be relied upon as constituting legal, financial or other professional advice. A professional advisor should be consulted regarding your specific situation. Information presented is believed to be factual and up-to-date but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. No endorsement of any third parties or their advice, opinions, information, products or services is expressly given or implied by Royal Bank of Canada or any of its affiliates.